You can create a customized template for a user with a company document viewer. In this template you specify which permissions the user is given.

Company document viewer template for accountants

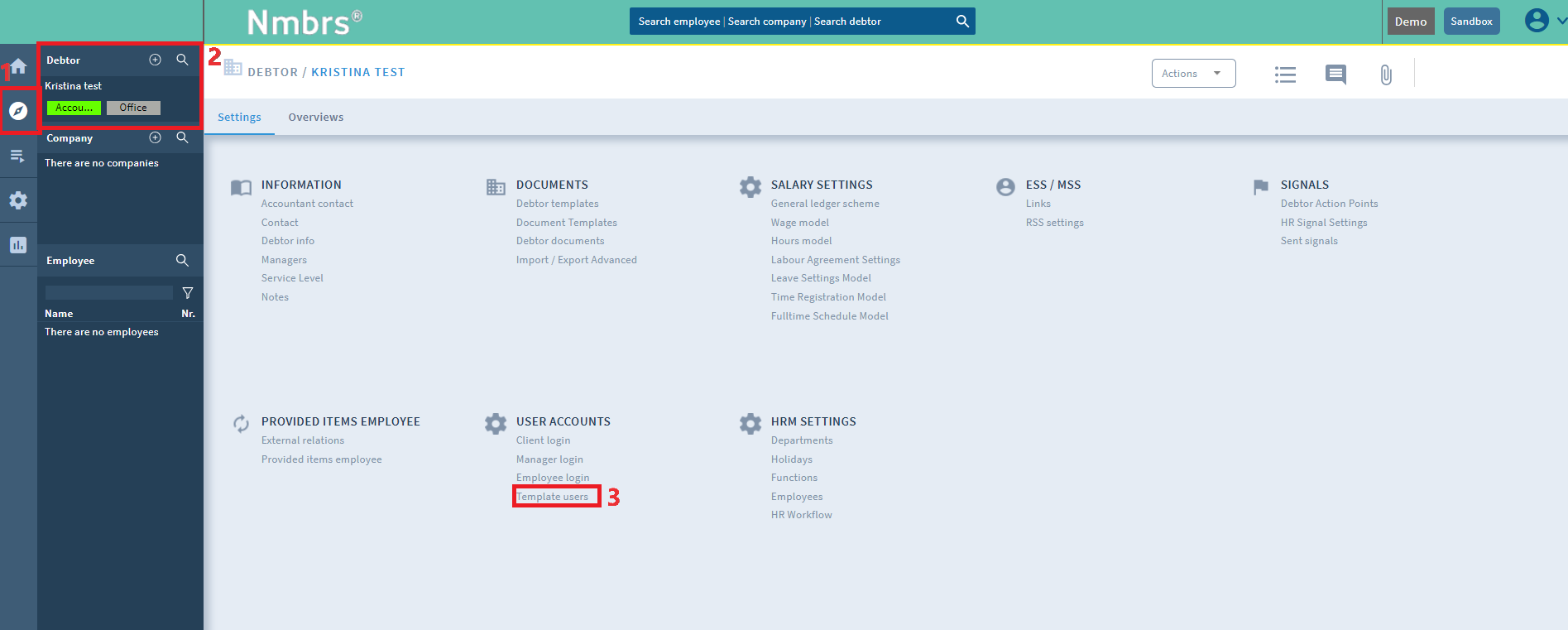

At debtor level in the 'Explorer' tab, you can create the company document viewer template under 'User templates'.

On the 'Settings' tab, you can also create user templates for all your debtors.

Company document viewer template for clients

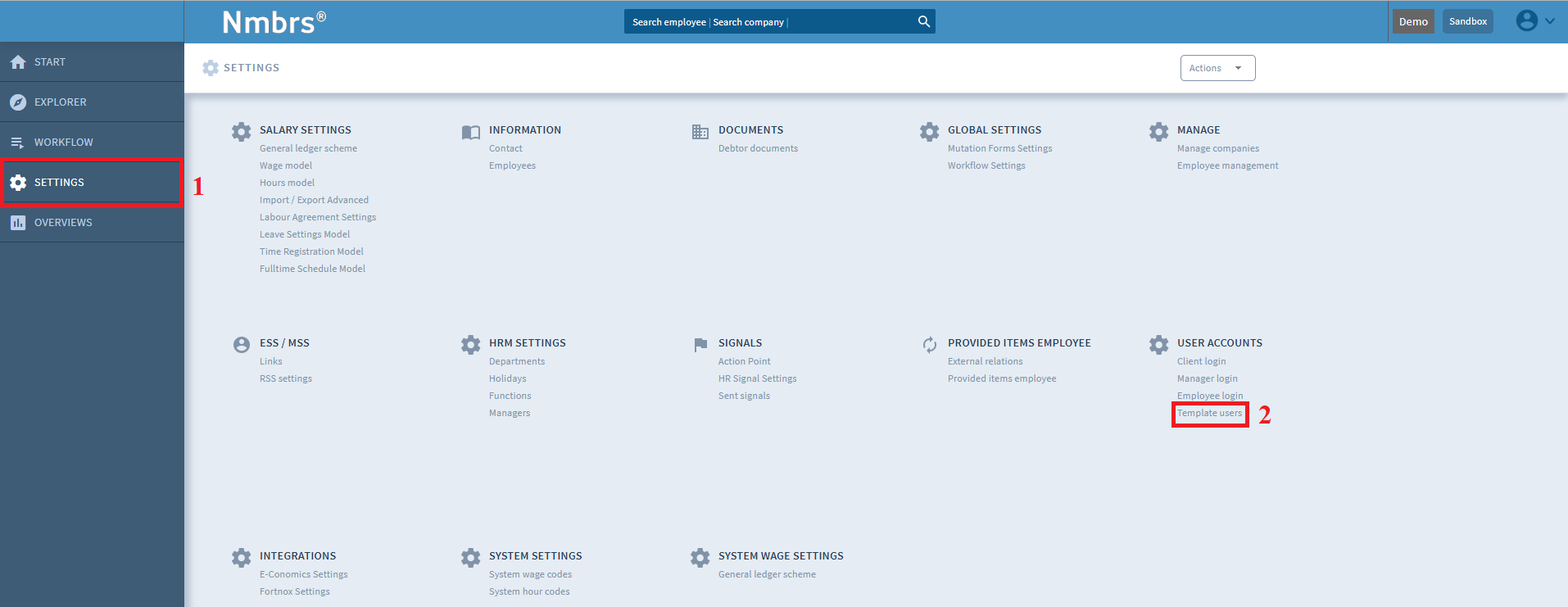

On the 'Settings' tab, you can create a company document viewer under 'User templates'.

New user template

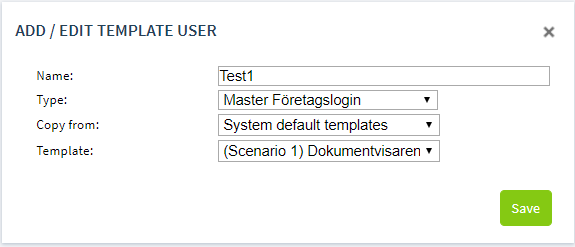

You can click on the button at the top left of your screen to create a new user template.

Base template

Enter a name for the template and select the type 'Master Company Login' and select if you want to copy the 'System default templates' . Select the 'Base Template Document Viewer' here to create a template.

Dashboard

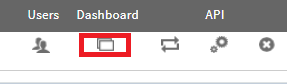

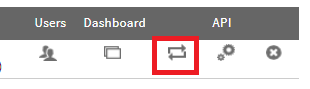

Next to the newly created template are 4 icons. Click on the second icon to open the dashboard editor.

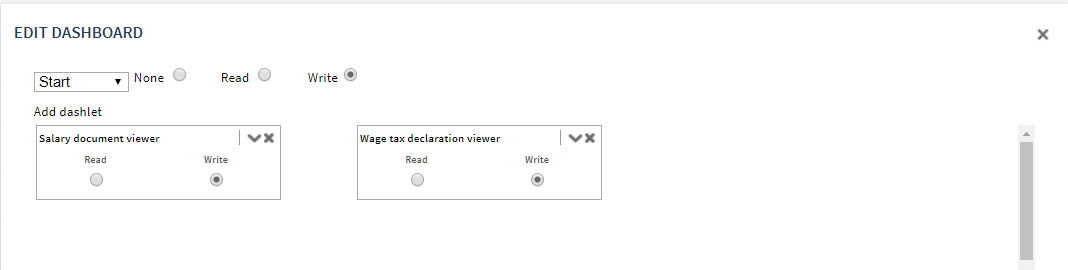

Assigning Read and Write permissions

- Salary document viewer Read rights: The user has permission to view Payroll documents, such as Journal entries and payment files. You can choose which salary documents the user can see at company level. This will be discussed later.

- Wage tax declaration viewer Read rights: The user has permission to view the created and sent wage tax declaration.

- Wage tax declaration viewer Write permission: The user has permission to send the wage tax declaration to the Tax authorities himself.

Apply template

When you have already applied this template to a user and this template has been changed, click on the third icon: Apply template.

If you have not yet assigned this template to a user, you do not have to do this.

Salary document settings

At company level in the 'Salary documents settings' dashlet, you can select the salary documents which you want to make visible in the document viewer.

Changing visible documents

With the 'Change visible documents' button you can select the documents which you want to make visible to the user.

Comments